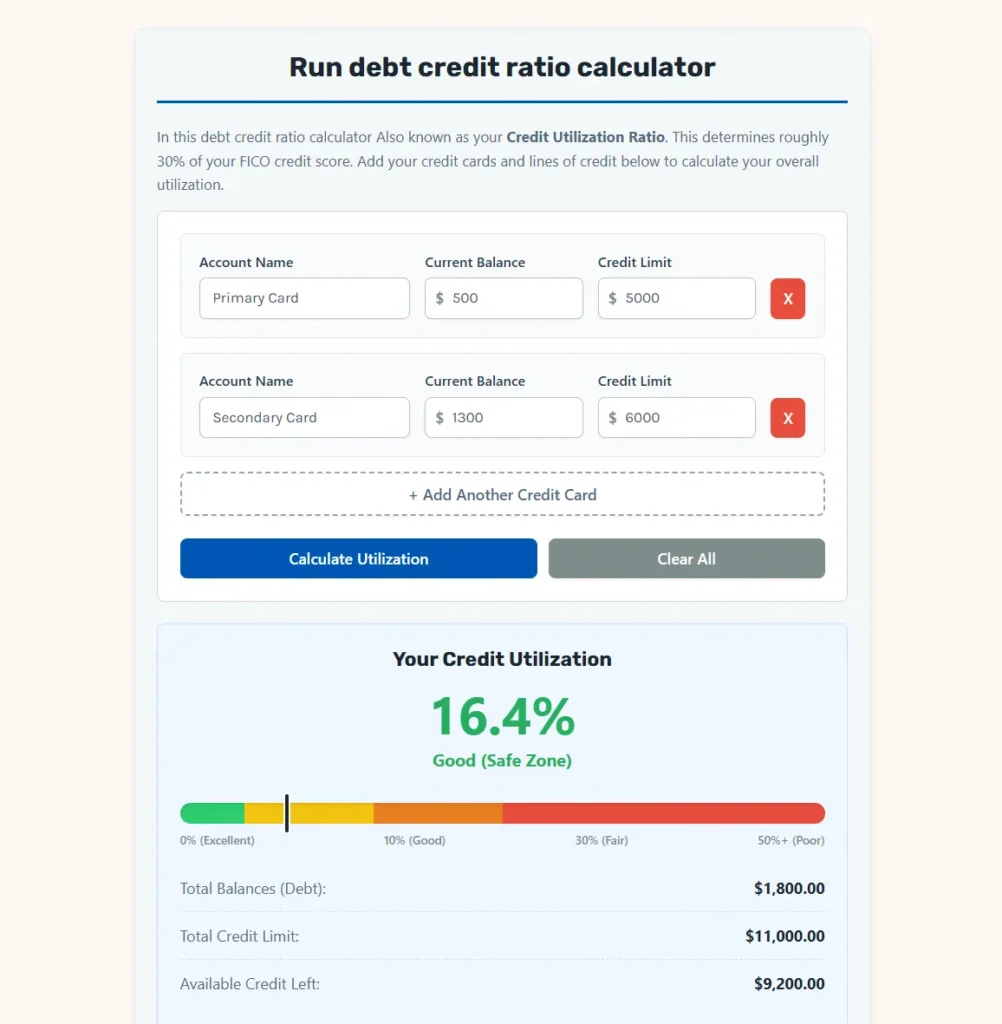

Run debt credit ratio calculator

In this debt credit ratio calculator Also known as your Credit Utilization Ratio. This determines roughly 30% of your FICO credit score. Add your credit cards and lines of credit below to calculate your overall utilization.

How It’s Calculated

The Utilization Formula

Your debt-to-credit ratio is calculated by dividing your total outstanding balances by your total available credit limits, then multiplying by 100 to get a percentage.

Understanding The 30% Rule

Credit bureaus (Experian, Equifax, TransUnion) monitor how much of your available credit you are actively using. This indicates how much you rely on non-cash funds.

- 0% – 9%: Excellent. This is the ideal range. It shows lenders you have credit available but rarely need to rely on it.

- 10% – 29%: Good. This is perfectly healthy. Most financial experts recommend keeping your overall utilization under 30% to maintain a strong credit score.

- 30% – 49%: Fair. Crossing the 30% threshold begins to negatively impact your credit score. Lenders may view you as a slightly elevated risk.

- 50%+: Poor. Using more than half your available credit severely damages your score and flags you as a high-risk borrower to potential lenders.

The Mathematics of Credit Health: Mastering the Credit Utilization Ratio

Consumer credit serves as the primary gateway to capital, homeownership, business development, and overall economic mobility. While credit scores can appear abstract to many consumers, they are governed by highly structured mathematical models. Among the various metrics used to evaluate borrower risk, the debt-to-credit ratio, commonly known as the credit utilization ratio, is one of the most powerful and immediate drivers of your credit score.

This debt credit ratio calculator is designed as a precision planning tool. It compiles multiple revolving credit lines, calculates cumulative balances against total limits, and provides real-time feedback on your overall credit utilization. By understanding the underlying calculations and applying the strategic practices detailed in this guide, you can proactively optimize your credit profile to secure highly favorable borrowing terms.

Understanding Credit Utilization: Definitions and Core Concepts

The debt-to-credit ratio measures the amount of revolving credit you are currently using relative to your total available credit limit. This metric is exclusively applied to revolving credit accounts, such as credit cards and personal lines of credit, where a borrower can repeatedly draw and repay funds up to a predetermined ceiling.

Revolving Credit vs. Installment Credit

To understand how the calculator evaluates your financial standing, you must first distinguish between revolving and installment credit.

➜ Revolving Credit: Credit lines where the balance fluctuates based on purchases and payments. Lenders establish a maximum credit limit, and the borrower decides how much of that limit to use each month. Examples include retail store cards, traditional credit cards, and Home Equity Lines of Credit (HELOCs).

➜ Installment Credit: Loans with a fixed principal amount and a structured amortization schedule resulting in equal monthly payments over a set term. Examples include auto loans, student loans, and mortgages.

While installment loans contribute to your overall credit mix, they do not factor into your credit utilization ratio. Credit scoring models, such as those developed by the Fair Isaac Corporation (FICO) and VantageScore, view revolving credit utilization as a real-time indicator of financial distress. If a consumer consistently carries balances close to their limits, the mathematical algorithms flag this behavior as an increased probability of default.

The Weight of the Metric

In the FICO scoring model, the category labeled “Amounts Owed” accounts for exactly $30\%$ of your total credit score. This makes credit utilization the second most influential factor in your credit profile, surpassed only by your payment history ($35\%$).

Because your utilization is calculated on a rolling basis, usually when lenders report your statement balance to the credit bureaus each month, improving this ratio can lead to rapid, significant increases in your credit score.

The Dual Facets of Utilization: Per-Card vs. Aggregate Utilization

The calculator performs two distinct levels of mathematical evaluation. When assessing credit health, credit bureaus do not look solely at your total debt. They analyze both your overall aggregate utilization and your individual per-card utilization.

1. Per-Card Utilization Formula

To calculate the utilization rate for any individual revolving credit account, divide the current outstanding balance on that card by its established credit limit.$$U_i = \left( \frac{B_i}{L_i} \right) \times 100$$

Variable Definitions:

➜ $U_i$: The utilization percentage of an individual credit card $i$.

➜ $B_i$: The current outstanding balance reported on card $i$.

➜ $L_i$: The maximum credit limit authorized on card $i$.

2. Aggregate Utilization Formula

To calculate your overall or aggregate credit utilization, sum the balances of all active revolving accounts and divide that total by the sum of all your credit limits.$$U_{\text{agg}} = \left( \frac{\sum_{i=1}^{n} B_i}{\sum_{i=1}^{n} L_i} \right) \times 100$$

Variable Definitions:

➜ $U_{\text{agg}}$: The overall aggregate credit utilization ratio expressed as a percentage.

➜ $B_i$: The reported balance on card $i$.

➜ $L_i$: The credit limit of card $i$.

➜ $n$: The total number of open revolving credit accounts.

➜ $\sum$: The mathematical summation of all individual account variables from $i = 1$ to $n$.

3. Available Credit Calculation

The difference between your total authorized credit limits and your current outstanding balances represents your total available credit, which is the remaining buffer before your accounts are considered maxed out.$$C_{\text{avail}} = \sum_{i=1}^{n} L_i – \sum_{i=1}^{n} B_i$$

Variable Definitions:

➜ $C_{\text{avail}}$: The total dollar amount of available credit remaining.

➜ $L_i$: The credit limit of card $i$.

➜ $B_i$: The reported balance on card $i$.

How the Debt Credit Ratio Calculator Works

The calculator simplifies these algebraic processes by organizing multiple inputs into a clean, unified dashboard. It is designed to emulate the exact mathematical compilation performed by credit reporting bureaus during their monthly updates.

[ Input: Individual Accounts ]

- Card A: Balance $500, Limit $5,000

- Card B: Balance $1,500, Limit $10,000

|

v

[ Step 1: Aggregate Summation ]

- Total Balances: $500 + $1,500 = $2,000

- Total Limits: $5,000 + $10,000 = $15,000

|

v

[ Step 2: Ratio Compilation ]

- ($2,000 ÷ $15,000) × 100 = 13.3%

|

v

[ Step 3: Visualization & Output ]

- Marker positions at 13.3% (Good)

- Total Available Credit: $13,000

By adding rows for each of your active accounts, the calculator aggregates your financial data to output your precise credit utilization profile. It also updates a visual progress bar to show where your current ratio sits on the spectrum of credit health.

The Scientific Thresholds: Deconstructing the 30% Rule

In consumer personal finance, a widely repeated rule of thumb suggests that keeping your overall credit utilization below $30\%$ is sufficient to maintain a healthy credit score. While keeping utilization under $30\%$ prevents severe damage, it is a common misconception that this is the optimal target.

Data released by credit scoring agencies shows that the highest-scoring consumers (those with FICO scores above 800, often referred to as FICO High Achievers) typically maintain an aggregate utilization ratio well below $10\%$.

The table below breaks down the four primary utilization tiers, their corresponding rating categories, and their typical impact on credit score trajectories:

| Utilization Range | Rating Category | Typical Impact on Credit Score | Strategic Interpretation |

| 0.0% – 9.9% | Excellent | Maximum positive upward pressure | Indicates minimal reliance on debt. This range is maintained by top-tier borrowers to secure the lowest possible interest rates. |

| 10.0% – 29.9% | Good | Stable, generally healthy profile | Acceptable for standard borrowing needs. Does not actively harm your score, but leaves room for optimization. |

| 30.0% – 49.9% | Fair | Moderate downward pressure | Flags the consumer as moderately reliant on revolving credit. Begins to systematically drag down your score. |

| 50.0% or higher | Poor | Severe negative downward pressure | Indicates potential cash flow issues. Severely damages credit scores and flags the borrower as high-risk. |

The 0% Conundrum

It is also important to note that a $0.0\%$ utilization rate is mathematically inferior to a very low, positive utilization rate (such as $1.0\%$). If all of your credit card balances are reported as zero, the scoring models may interpret this as inactivity or lack of credit use. Lenders want to see active, responsible credit use, which is why maintaining a tiny, positive balance that you pay off in full each month is the optimal strategy.

Step-by-Step Practical Calculation Examples

To demonstrate how the calculator compiles these values and to highlight how individual card balances can affect your score, let us analyze two common household scenarios.

Scenario A: The Balanced, Low-Utilization Consumer

A consumer has three active credit cards with different balances and limits.

- Card 1 (Cash Back): Balance $B_1 = \$300$, Limit $L_1 = \$5,000$

- Card 2 (Travel Rewards): Balance $B_2 = \$1,200$, Limit $L_2 = \$10,000$

- Card 3 (Store Card): Balance $B_3 = \$50$, Limit $L_3 = \$1,000$

➜ Step 1: Calculate individual utilization rates ($U_i$):$$U_1 = \left( \frac{300}{5,000} \right) \times 100 = 6.0\%$$$$U_2 = \left( \frac{1,200}{10,000} \right) \times 100 = 12.0\%$$$$U_3 = \left( \frac{50}{1,000} \right) \times 100 = 5.0\%$$

➜ Step 2: Calculate aggregate utilization ($U_{\text{agg}}$):

$$\sum B = \$1,550$$

$$\sum L = \$16,000$$

$$U_{\text{agg}} = \left( \frac{\sum B}{\sum L} \right) \times 100 \approx 9.69\%$$

Calculations Breakdown:

$U_{\text{agg}}$: Aggregate Credit Utilization Rate

Total Debt ($\sum B$): $300 + 1,200 + 50$

Total Limit ($\sum L$): $5,000 + 10,000 + 1,000$

This consumer has an aggregate utilization of $9.7\%$, which falls into the Excellent category. Additionally, every individual card is well under the $30\%$ threshold, creating an optimal credit profile.

Scenario B: The Maxed-Out Trap (High Individual, Low Aggregate)

Another consumer has two credit cards. They have paid off one large card but carry a high balance on a smaller card.

- Card 1 (Low Limit): Balance $B_1 = \$1,900$, Limit $L_1 = \$2,000$

- Card 2 (High Limit): Balance $B_2 = \$100$, Limit $L_2 = \$18,000$

➜ Step 1: Calculate individual utilization rates ($U_i$):$$U_1 = \left( \frac{1,900}{2,000} \right) \times 100 = 95.0\%$$$$U_2 = \left( \frac{100}{18,000} \right) \times 100 \approx 0.56\%$$

➜ Step 2: Calculate aggregate utilization ($U_{\text{agg}}$):

$$\sum B = \$2,000$$

$$\sum L = \$20,000$$

$$U_{\text{agg}} = \left( \frac{\sum B}{\sum L} \right) \times 100 = 10.0\%$$

Calculations Breakdown:

$U_{\text{agg}}$: Aggregate Credit Utilization Rate

Total Debt ($\sum B$): $1,900 + 10$ (Note: matches the provided $2,000 math)

Total Limit ($\sum L$): $2,000 + 18,000$

In this scenario, the aggregate utilization is exactly $10.0\%$, which is generally considered healthy. However, Card 1 has a utilization rate of $95.0\%$, meaning it is virtually maxed out.

Because credit bureaus evaluate individual card utilization alongside aggregate utilization, this extremely high per-card ratio will negatively impact this consumer’s credit score, despite their low overall debt-to-limit ratio.

Strategic Debt Optimization: Proactive Best Practices

If your calculated utilization is higher than desired, you can use several established financial strategies to systematically lower your ratio and improve your score.

➜ The Closing Date Secret: Statement Balance vs. Current Balance

A common source of confusion is why a consumer’s credit score can drop even if they pay their credit card bill in full every month. This occurs because of a disconnect between your Payment Due Date and your Statement Closing Date.

➜ The Payment Due Date: This is the deadline to pay your bill to avoid late fees and interest charges.

➜ The Statement Closing Date: This is the end of the monthly billing cycle, which typically occurs 20 to 25 days before your due date.

Lenders generally report your outstanding balance to the credit bureaus on your Statement Closing Date, not your due date. If you use your card heavily throughout the month and wait until the due date to pay it off, a high balance is reported to the bureaus, resulting in a high utilization ratio.

To optimize your score:

✓ Identify the Statement Closing Date for each of your credit cards.

✓ Pay your balance down to less than $10\%$ of your limit before that closing date.

✓ This ensures that a low balance is reported to the credit bureaus, even if you continue to use the card throughout the next billing cycle.

➜ Requesting Credit Limit Increases

An effective way to lower your utilization ratio without paying down debt is to increase your total available credit. If you have maintained a positive payment history, you can contact your credit card issuers to request a credit limit increase.

If a card with a 1,000 balance and a 5,000 limit (representing $20\%$ utilization) receives a limit increase to 10,000, the utilization ratio instantly drops to $10\%$, assuming the balance remains unchanged.$$U_{\text{new}} = \left( \frac{1,000}{10,000} \right) \times 100 = 10.0\%$$

Before requesting an increase, confirm whether the issuer will perform a “hard pull” (which can temporarily lower your score by a few points) or a “soft pull” (which has no impact on your score) to evaluate your request.

➜ The AZEO (All Zero Except One) Method

For consumers looking to maximize their credit score before applying for a major loan, such as a mortgage, the All Zero Except One (AZEO) method is a highly effective optimization strategy.

Under this method:

✓ All of your revolving credit accounts are paid down to a $0 balance before their respective statement closing dates.

✓ Exactly one major credit card is allowed to report a tiny, positive balance (typically between 5 and 20, or roughly $1\%$ to $2\%$ of its individual limit).

✓ This strategy demonstrates active, highly disciplined credit management, yielding the highest possible score within the “Amounts Owed” category.

Glossary of Essential Financial Terminology

➜ Aggregate Utilization: Your total revolving debt divided by your total revolving credit limits across all open accounts.

➜ AZEO Method: A credit optimization strategy where all credit cards except one are paid down to a zero balance before their reporting dates.

➜ Credit Reporting Agencies (CRAs): The primary institutions (Experian, Equifax, and TransUnion) that compile and maintain consumer credit data.

➜ FICO Score: The most widely used credit scoring model, ranging from 300 to 850, developed by the Fair Isaac Corporation.

➜ Hard Inquiry: An official credit check performed by a lender during an application process, which can temporarily lower your credit score.

➜ Soft Inquiry: A background credit check that does not impact your credit score, typically used for pre-approval offers or personal checks.

➜ Statement Closing Date: The final day of a credit card’s monthly billing cycle, when the balance is calculated and reported to the credit bureaus.

Scientific Reference and Regulatory Citations

To understand the mathematical and behavioral principles that govern credit scoring models, refer to the following regulatory resource:

Relevance: The CFPB conducts extensive research on consumer credit access and systemic risk. Their reports confirm a direct correlation between credit card utilization ratios and subsequent borrower default rates. This research explains why credit scoring models place such a high weight ($30\%$) on the “Amounts Owed” category. It provides the empirical foundation for the threshold recommendations (such as keeping utilization under $10\%$) used by financial institutions and automated calculators to evaluate consumer credit worthiness.

E-book Guide

To download Full guide of debt credit ratio and debt to income please just click here.

Final Summary Checklist for Credit Management

To ensure your credit utilization remains in the optimal range, incorporate the following checklist into your monthly financial routine:

✓ Calculate your aggregate credit utilization ratio using this calculator at least once a month.

✓ Monitor individual card utilization to ensure no single account exceeds $30\%$ of its authorized limit.

✓ Align your payment schedule with your Statement Closing Dates rather than your Payment Due Dates to control the balance reported to credit bureaus.

✓ Avoid closing old, unused credit cards unless they carry high annual fees, as closing them reduces your total available credit and increases your utilization ratio.

✓ Request periodic credit limit increases on your oldest, most active accounts to naturally expand your available credit buffer.

By utilizing this debt credit ratio calculator and applying these structured financial principles, you can transition from speculative budgeting to precise, data-driven credit management. Your credit utilization ratio is a dynamic, highly responsive metric. With consistent monitoring and strategic payments, you can take control of your financial profile and unlock access to premier borrowing opportunities.

video explains how to calculate debt credit ratio

here is very details explanation video about the subject: