Run Property Depreciation Calculator

In this Property Depreciation Calculator Analyze and calculate standard tax depreciation deductions for commercial or residential real estate. Plan real estate investments based on the asset’s recovery period and placement date.

Property Tax Depreciation Explained

Fundamental Tax Depreciation Equations

Under tax frameworks, properties are separated into land elements and structural improvements. Only structural improvements suffer wear and tear, and are therefore eligible for depreciation calculations:

Depreciable Basis = Purchase Price − (Purchase Price × Land Percentage)

Annual Straight-Line Deduction = Depreciable Basis / Useful Life (Years)

The Mid-Month Convention dictates that regardless of which day of the month an asset is placed in service, it is considered placed in service exactly in the middle of that month, granting a prorated portion of depreciation for Year 1:

Year 1 Fraction = (12.5 − Month Placed) / 12

Recovery Timelines Reference

Standard Periods for Real Estate Investments

- Residential Income Property (27.5 Years): Single-family rentals, apartment structures, duplexes, and multi-family structures.

- Commercial Income Property (39 Years): Warehouses, medical structures, office buildings, storefronts, and industrial infrastructure.

- Land Improvements (15 Years): Exterior features including fences, driveways, sidewalks, and agricultural drainage frameworks.

- Qualified Business Assets (5 Years): Computers, office tech systems, appliances, and localized enterprise equipment assets.

The Architecture of the Tax Shield: Mastering Property Depreciation Economics

Real estate investment is as much about structural tax efficiency as it is about physical rental yields and capital appreciation. To the untrained eye, property represents a single, solid physical asset. To tax authorities, corporate accountants, and financial planners, however, a real estate purchase is a modular system composed of non-depreciable land, depreciable structural improvements, and high-velocity personal property assets.

This property depreciation guide serves as an authoritative framework to understand how the raw cost of real property is systematically recovered over its useful regulatory lifespan. By translating property acquisitions into multi-decade tax-saving projections, investors can construct an optimal financial shield that protects operational cash flows from excessive taxation.

Understanding Property Depreciation: Concept and Definition

At its core, depreciation is an accounting system designed to match the economic cost of an asset’s physical wear, tear, and obsolescence with the revenues that the asset generates over its operational lifetime. In the context of real estate, the concept is grounded in physical reality: while the land beneath a structure remains permanent, the physical structures themselves gradually decay. Roofs degrade, mechanical systems fail, foundations settle, and internal finishes wear down.

From a tax perspective, this physical degradation represents a real, deductible economic expense. However, unlike standard operating expenses such as property management fees, landlord insurance, or utility bills, depreciation is classified as a non-cash expense. The property owner does not write a monthly or annual check for depreciation. Instead, they deduct a portion of the building’s historical cost from their taxable rental income each year.

This mechanism reduces net taxable income while leaving the underlying physical cash flow untouched. The result is a highly effective tax shield. For profitable investments, this structural shield can turn a positive cash-flowing rental property into a paper loss for tax reporting purposes, allowing the owner to defer or completely avoid tax liabilities during the holding period.

The Crucial Separation of Land and Structural Improvements

A fundamental axiom of tax depreciation is that physical land cannot be depreciated. Land does not suffer wear, tear, or chronological decay, and it possesses an indefinite useful life. Therefore, when a real estate asset is acquired, the investor must divide the total purchase price into two distinct allocations: the non-depreciable land value and the depreciable improvements value.

Determining this percentage allocation must be handled with strict analytical accuracy. Over-allocating value to the building to inflate depreciation deductions is a primary trigger for regulatory audits, while under-allocating leaves substantial tax savings on the table. To establish a defensible depreciable basis, real estate professionals utilize three main valuation methodologies:

- The Property Assessor Ratio Method: This approach utilizes the assessment ratio provided by the local county property tax appraiser. If the tax assessor values the land at 100,000 and the building at 400,000, the building improvements represent 80 percent of the total value. This 80 percent allocation ratio is then applied directly to the investor’s actual purchase price.

- The Licensed Appraisal Method: A licensed, independent real estate appraiser determines the replacement cost of the physical improvements or assigns a specific land-only value based on local comparable sales of vacant parcels. The remaining residual value of the purchase price is allocated to the building.

- The Replacement Cost Method: A qualified structural engineer or general contractor calculates the exact cost required to reconstruct the physical building from scratch using modern building materials. This calculated replacement cost is established as the depreciable improvements basis, with the balance of the transaction price attributed to the underlying land.

Mathematical Formulations of Real Estate Depreciation

To understand how a depreciation schedule is compiled over time, we must examine the algebraic formulations that drive the calculations. These formulas reflect the standard equations used in corporate accounting and the Modified Accelerated Cost Recovery System (MACRS).

1. Calculating the Depreciable Asset Basis

The depreciable basis represents the total dollar value of the physical improvements subject to tax depreciation. It is calculated by stripping away the land value from the historical acquisition cost:$$B = P \times \left(1 – \frac{L}{100}\right)$$

Where:

- $B$ = Depreciable Asset Basis (expressed in dollars)

- $P$ = Total Property Purchase Price (including capitalized acquisition costs such as legal fees, transfer taxes, and title insurance)

- $L$ = Land Allocation Percentage (the portion of the purchase price allocated to the non-depreciable land)

2. The Annual Straight-Line Depreciation Deduction

Under the straight-line method, the depreciable basis is recovered evenly over the asset’s assigned regulatory recovery period. For each full calendar year the property is in service, the deduction remains constant:$$D_{\text{annual}} = \frac{B}{N}$$

Where:

- $D_{\text{annual}}$ = Standard full-year depreciation deduction (expressed in dollars)

- $B$ = Depreciable Asset Basis

- $N$ = Recovery Period or Useful Life (expressed in years, e.g., 27.5 years for residential rental, 39 years for commercial)

3. The Mid-Month Convention and Year 1 Fraction

Under MACRS guidelines, real property is subject to the Mid-Month Convention. This rule dictates that regardless of the exact calendar day a property is placed in service, it is legally treated as having been placed in service exactly in the middle of that month.

Consequently, the property owner receives a half-month of depreciation for the acquisition month, plus full monthly allocations for any subsequent months in that first tax year:$$F_{\text{year 1}} = \frac{12.5 – M}{12}$$

Where:

- $F_{\text{year 1}}$ = Proration factor applied to the first tax year’s depreciation deduction (expressed as a decimal)

- $M$ = Chronological month in which the property was placed in service (where January = 1, May = 5, December = 12)

- $12.5$ = Regulatory constant representing the half-month credit allocated to the startup month

4. The Year 1 Prorated Depreciation Deduction

By combining the straight-line rate with the mid-month proration factor, we arrive at the first year’s allowable deduction:$$D_{\text{year 1}} = \frac{B}{N} \times F_{\text{year 1}}$$

Where:

- $D_{\text{year 1}}$ = Permitted depreciation deduction for the initial partial tax year (expressed in dollars)

Step-by-Step Practical Scenario: A Comprehensive Case Study

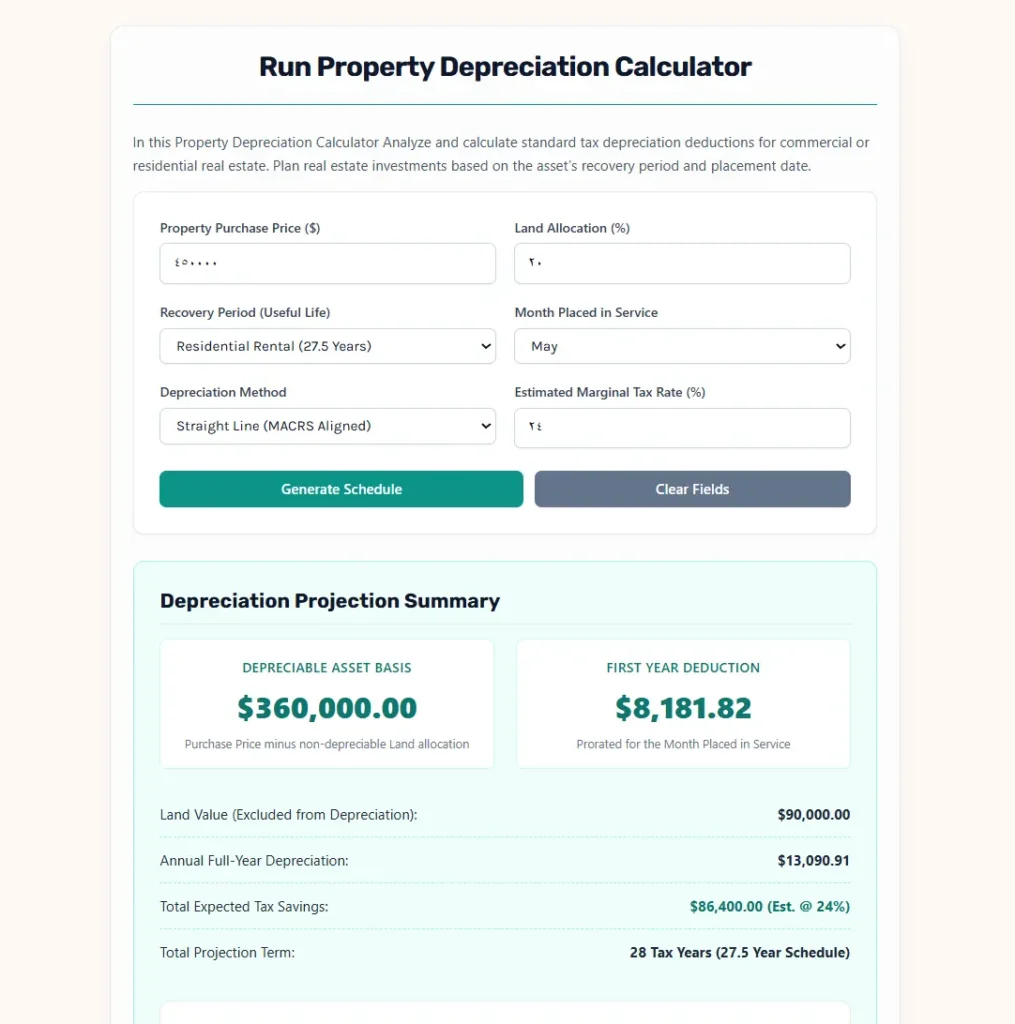

To see how these formulas function in a practical scenario, let us execute a complete step-by-step calculation for a typical residential rental property acquisition using the standard parameters.

Initial Parameters:

- Property Purchase Price ($P$): $450,000

- Land Allocation ($L$): 20%

- Useful Life / Recovery Period ($N$): 27.5 Years (Residential Rental)

- Month Placed in Service ($M$): May (Month 5)

- Marginal Tax Rate: 24%

- Method: Straight Line (MACRS Aligned)

Step 1: Isolate the Depreciable Asset Basis ($B$)

To remove the land value, we calculate the building improvement value:$$B = \$450,000 \times \left(1 – \frac{20}{100}\right)$$$$B = \$450,000 \times 0.80$$$$B = \$360,000$$

$\rightarrow$ The land value is isolated at 90,000 and is excluded from the depreciation schedule. The depreciable basis of the building is exactly $360,000.

Step 2: Determine the Annual Full-Year Depreciation Deduction ($D_{\text{annual}}$)

Next, we calculate the standard deduction for a full calendar year of ownership:$$D_{\text{annual}} = \frac{\$360,000}{27.5}$$$$D_{\text{annual}} \approx \$13,090.91$$

$\rightarrow$ In a standard, full twelve-month tax year, the property will yield a depreciation write-off of exactly $13,090.91.

Step 3: Calculate the Year 1 Proration Factor ($F_{\text{year 1}}$) using the Mid-Month Convention

Because the property was placed in service in May (Month 5), we calculate the prorated fraction of the year:$$F_{\text{year 1}} = \frac{12.5 – 5}{12}$$$$F_{\text{year 1}} = \frac{7.5}{12}$$$$F_{\text{year 1}} = 0.625$$

$\rightarrow$ The property is eligible for 62.5 percent of a full year’s depreciation during its first tax year. This corresponds to exactly 7.5 months of service (7 full months from June through December, plus 0.5 months for the month of May).

Step 4: Calculate the Initial Year 1 Deduction ($D_{\text{year 1}}$)

Applying the proration factor to the annual rate gives the initial tax deduction:$$D_{\text{year 1}} = \$13,090.91 \times 0.625$$$$D_{\text{year 1}} \approx \$8,181.82$$

$\rightarrow$ The tax deduction for the first partial year of ownership is exactly $8,181.82.

Step 5: Draft the Multi-Year Amortization Schedule

Because the initial year was prorated, the depreciation schedule must extend into an additional tax year to recover the remaining basis. The schedule spans 29 tax years:

- Year 1 (Prorated): $8,181.82

- Years 2 through 28 (27 Full Years): 13,090.91 per year (totaling $353,454.57)

- Year 29 (Remaining Remainder): Calculated as the residual basis left to recover:

$$D_{\text{year 29}} = B \times \frac{1}{N} \times (1 – F_{\text{year 1}})$$$$D_{\text{year 29}} = \$13,090.91 \times (1 – 0.625)$$$$D_{\text{year 29}} = \$13,090.91 \times 0.375 \approx \$4,909.09$$

- Total Basis Recovered: $\$8,181.82 + \$353,454.57 + \$4,909.09 = \$360,000.00$

Step 6: Determine Expected Nominal Tax Savings

By writing off 360,000 against income taxed at a marginal rate of 24 percent, the property owner realizes substantial total nominal tax savings over the life of the asset:$$\text{Tax Savings} = \$360,000 \times 0.24 = \$86,400$$

$\rightarrow$ This represents $86,400 in direct, cumulative cash kept in the investor’s pocket rather than paid in federal income taxes.

MACRS Asset Classifications and Recovery Timelines

Under the Modified Accelerated Cost Recovery System, the IRS designates standard recovery periods for different types of investments. Accurate classification prevents audit exposure and ensures structural alignment with tax code guidelines:

| Asset Classification | Useful Life (N) | Calculation Convention | Qualified Structural Components and Examples |

| Residential Rental | 27.5 Years | Mid-Month | Single-family rental houses, apartment buildings, duplexes, triplexes, townhomes, and student housing. |

| Commercial Property | 39.0 Years | Mid-Month | Retail stores, shopping plazas, warehouses, medical offices, manufacturing plants, and corporate spaces. |

| Land Improvements | 15.0 Years | Half-Year / Mid-Quarter | Physical improvements outside the building footprint, including fences, sidewalks, driveways, parking lots, and shrubbery. |

| Qualified Business Property | 5.0 Years | Half-Year / Mid-Quarter | Personal property inside the rental unit, including laundry machines, refrigerators, office computers, and specialized machinery. |

Strategic Tax Optimization: Cost Segregation and Bonus Depreciation

Sophisticated real estate investors do not view depreciation as a static, passive process. Instead, they use advanced planning tools to accelerate their deductions, shifting tax write-offs from the distant future into the immediate present.

Cost Segregation Studies

Although a residential building is depreciated over a standard 27.5-year cycle, the building is physically composed of many shorter-lived systems. A Cost Segregation Study is an engineering and accounting analysis that dissects a real estate acquisition into its individual components.

By identifying elements that can be reclassified as 15-year land improvements or 5-year personal property, the investor can front-load depreciation deductions. For example, carpet, specialty lighting, decorative millwork, security systems, and perimeter fencing can be peeled away from the 27.5-year structural classification and depreciated rapidly.

The Time Value of Money (TVM) Benefit

Accelerating depreciation is highly advantageous due to the time value of money. A dollar saved in taxes today is worth significantly more than a dollar saved twenty years from now. By maximizing deductions in the initial years of ownership, investors can reinvest the tax savings back into their real estate portfolio, paying down debt or acquiring additional income-producing assets.

The Cost of Real Estate Sales: Depreciation Recapture

While depreciation provides a powerful tax shield during the ownership phase, investors must prepare for its eventual financial impact upon sale. This impact is known as Section 1250 Depreciation Recapture.

When a property is sold for more than its depreciated book value, the IRS seeks to recover the tax benefits previously enjoyed by the owner. The accumulated depreciation deductions are subject to a specialized tax known as the depreciation recapture tax, which is capped at a maximum rate of 25 percent.

For example, if an investor claimed 100,000 in cumulative depreciation deductions over a ten-year hold, they must pay up to $25,000 in recapture taxes upon sale, regardless of their standard capital gains tax bracket.

Strategic Deferral via the Section 1031 Exchange

To bypass the immediate impact of depreciation recapture, real estate investors frequently use Section 1031 of the Internal Revenue Code. A 1031 Exchange allows a property owner to defer both their capital gains taxes and their depreciation recapture taxes by selling their current investment property and reinvesting the entire proceeds into a replacement property of “like-kind.”

By executing a continuous chain of 1031 exchanges over a lifetime, an investor can defer recapture taxes indefinitely, allowing their wealth to compound uninterrupted.

Best Practices for Real Estate Investors

To ensure maximum financial efficiency and full regulatory compliance, real estate owners should integrate the following best practices into their tax planning workflow:

- Retain Detailed Closing Statements: Always keep copies of your HUD-1 or ALTA settlement statements. Capitalized acquisition costs, such as title insurance, legal fees, and recording costs, must be added directly to your property basis.

- Obtain a Written Valuation Appraisal: Do not rely on casual online property estimates to determine your land-to-building allocation. Secure a professional property tax appraisal or assessor breakdown to establish a rock-solid, auditable paper trail.

- Differentiate Repairs from Capital Improvements: Routine maintenance costs, such as fixing a leaky pipe or patching a roof tile, must be expensed immediately in the year they occur. Major restorations, such as replacing an entire HVAC system or installing a brand-new roof, must be capitalized and depreciated over their corresponding MACRS useful life.

- Coordinate with a Certified Public Accountant (CPA): Real estate tax laws are highly complex and subject to change. Always review your depreciation schedules, cost segregation studies, and 1031 exchange plans with a qualified tax professional to ensure compliance with current federal, state, and local regulations.

Scientific Reference and Official Citation

For authoritative guidance, regulatory definitions, and the official mathematical frameworks underlying real property cost recovery schedules, refer directly to the primary governing administrative resource:

- Source: Internal Revenue Service (IRS), United States Department of the Treasury.

- Official Document: Publication 946: How To Depreciate Property.

- Relevance: Publication 946 is the official federal regulatory manual detailing MACRS classification codes, recovery period guidelines, the application of conventions (such as mid-month, mid-quarter, and half-year), and the statutory percentage tables used to compile compliant depreciation schedules.