Run Solar Loan Calculator

In this Solar Loan Calculator Determine your estimated monthly solar panel payments, uncover hidden interest costs, and calculate the true net cost of your system.

Understanding Solar Financing

How is the monthly payment calculated?

This calculator uses standard loan amortization. The formula determines a fixed monthly payment that ensures the entire principal amount and the accrued interest are paid off exactly by the end of the loan term.

M = P [ r(1 + r)n ] / [ (1 + r)n – 1 ]

- M = Total Monthly Payment

- P = Principal Loan Amount (Cost − Down Payment − Incentives)

- r = Monthly Interest Rate (Annual Rate ÷ 12)

- n = Number of Months (Years × 12)

A Note on Solar Tax Credits

Many countries offer tax credits (like the 30% Federal ITC in the US). In reality, you don’t receive this money until you file your taxes. Some solar lenders offer a “recast” loan: they front you the money for the first 12-18 months based on the lower net price, but if you don’t apply your tax credit to the loan by a specific date, your monthly payments will spike. This calculator assumes you are applying the credits upfront to reduce the base loan size.

Solar Photovoltaic Financing: Mathematical Foundations, Amortization Mechanics, and Investment Valuation

In the transition toward sustainable distributed energy infrastructure, the installation of residential and commercial solar photovoltaic (PV) systems has emerged as a primary capital investment. While transitioning away from traditional utility providers reduces monthly operating costs, the upfront acquisition of solar hardware requires a robust capital budgeting strategy. For most property owners, executing this transition involves securing dedicated solar financing.

A specialized solar loan calculator serves as an essential financial planning and underwriting tool. By integrating gross equipment costs, upfront down payments, statutory tax credits, interest rates, and amortization timelines, these calculators allow consumers, financiers, and contractors to model long-term cash flows. This guide provides an exhaustive analysis of the mathematical formulations, accounting principles, tax credit Recasting structures, and real-world scenarios that define professional solar financing.

Understanding the Financial Model of Solar Energy Adoption

To evaluate the mathematical models used to amortize solar loans, we must first examine the broader financial framework of solar energy adoption. Unlike consumer loans secured for depreciating assets, a solar loan is an investment in a productive, yield-generating asset. Solar panels generate electricity, which directly offsets an expense that the property owner would otherwise be obligated to pay to a monopolized utility company.

This dynamic creates several unique financial realities:

$\checkmark$ The Substitution Effect: Monthly solar loan payments do not represent a new expense. Instead, they substitute a variable, inflationary utility bill with a fixed, predictable financing payment that eventually terminates.

$\checkmark$ Asset Appreciation: Research indicates that owned solar installations appreciate the underlying real estate value, as the property boasts permanently lowered operating costs.

$\checkmark$ Statutory Subsidies: Governments frequently subsidize solar installations using direct tax credits, accelerated depreciation schedules, or local clean energy grants. This reduces the true net capital required to fund the system.

Deconstructing the Components of a Solar Loan

To run a reliable solar loan amortization model, an analyst must extract and evaluate five primary financial variables from a solar installation contract.

1. Gross System Cost

This is the total turn-key cost of the solar installation before any incentives, down payments, or tax credits are applied. It includes engineering, permitting, solar panels, inverters, racking, electrical upgrades, structural reinforcement, and installation labor.

2. Down Payment

The initial equity contribution made by the property owner at the time of contract execution. This capital directly reduces the initial principal balance of the loan.

3. Tax Credits and Upfront Incentives

Direct financial subsidies that are applied to reduce the net principal of the loan. The most prominent example is the federal Investment Tax Credit (ITC), which currently provides a substantial percentage-based reduction in net system liabilities.

4. Loan Term (Duration)

The length of time allocated to fully amortize the loan principal through regularly recurring payments. This is modeled in years but converted to months for monthly payment calculations.

5. Annual Interest Rate

The nominal interest rate charged by the lender, expressed as an annual percentage. This represents the cost of borrowing capital and is converted to a monthly periodic rate for amortization modeling.

The Mathematical Architecture of Solar Loan Amortization

To ensure perfect display on narrow mobile viewports and small screen content boxes, standard multi-variable amortization equations have been factored into single-step, vertically stacked formulations.

1. Net Principal Calculation

The net loan principal represents the total debt capital that must be borrowed to fund the system after accounting for upfront equity and direct subsidies.

The equation is:$$P = G – D – C$$

Where:

- $\rightarrow$ $P$ represents the Net Loan Principal.

- $\rightarrow$ $G$ represents the Gross System Cost.

- $\rightarrow$ $D$ represents the Down Payment.

- $\rightarrow$ $C$ represents the Upfront Tax Credits and Incentives.

2. Monthly Interest Rate Conversion

To calculate monthly payments, the nominal annual interest rate must be converted into a periodic monthly decimal rate.

The equation is:$$r = \frac{i}{1200}$$

Where:

- $\rightarrow$ $r$ represents the periodic Monthly Interest Rate as a decimal.

- $\rightarrow$ $i$ represents the nominal Annual Interest Rate (expressed as a percentage, such as $5.9$ for $5.9\%$).

- $\rightarrow$ $1200$ represents the conversion factor ($12\text{ months} \times 100\%$ scaling).

3. Total Payments Conversion

The loan term in years must be converted into the total number of monthly payments.

The equation is:$$n = t \times 12$$

Where:

- $\rightarrow$ $n$ represents the total number of Monthly Payments.

- $\rightarrow$ $t$ represents the Loan Term in Years.

- $\rightarrow$ $12$ represents the number of months in a year.

4. Amortization Growth Factor

To simplify the final monthly payment equation for narrow mobile screens, we isolate the compounding growth factor ($K$) of the periodic interest.

The equation is:$$K = (1 + r)^n$$

Where:

- $\rightarrow$ $K$ represents the Amortization Growth Factor.

- $\rightarrow$ $r$ represents the Monthly Interest Rate as a decimal.

- $\rightarrow$ $n$ represents the total number of Monthly Payments.

5. Monthly Payment Calculation

Using the isolated growth factor ($K$), the fixed monthly payment ($M$) required to amortize the loan is calculated using standard periodic compounding.

The equation is:$$M = P \times \left( \frac{r \times K}{K – 1} \right)$$

Where:

- $\rightarrow$ $M$ represents the Estimated Monthly Payment.

- $\rightarrow$ $P$ represents the Net Loan Principal.

- $\rightarrow$ $r$ represents the periodic Monthly Interest Rate as a decimal.

- $\rightarrow$ $K$ represents the Amortization Growth Factor.

6. Monthly Payment for 0% Interest Loans (Edge Case)

In scenarios where promotional $0\%$ financing is secured, the standard compounding formula results in division by zero. In these cases, the monthly payment is a simple division of principal over time.

The equation is:$$M_{0} = \frac{P}{n}$$

Where:

- $\rightarrow$ $M_{0}$ represents the Monthly Payment under $0\%$ interest.

- $\rightarrow$ $P$ represents the Net Loan Principal.

- $\rightarrow$ $n$ represents the total number of Monthly Payments.

7. Total Cumulative Cost of the Loan

The total lifetime cost of the loan represents the aggregate of all monthly payments made over the duration of the term.

The equation is:$$T_{\text{cost}} = M \times n$$

Where:

- $\rightarrow$ $T_{\text{cost}}$ represents the Total Lifetime Cost of the loan.

- $\rightarrow$ $M$ represents the calculated Monthly Payment.

- $\rightarrow$ $n$ represents the total number of Monthly Payments.

8. Total Interest Liabilities

The total interest paid over the life of the loan is the difference between the total payments and the borrowed principal.

The equation is:$$I_{\text{total}} = T_{\text{cost}} – P$$

Where:

- $\rightarrow$ $I_{\text{total}}$ represents the Total Interest Paid.

- $\rightarrow$ $T_{\text{cost}}$ represents the Total Lifetime Cost of the loan.

- $\rightarrow$ $P$ represents the Net Loan Principal.

The Solar Tax Credit and Loan Recasting Mechanics

A critical feature of residential solar loans is the relationship between the loan amortization schedule and government tax incentives. In the United States, the Residential Clean Energy Credit (often called the solar Investment Tax Credit or ITC) allows homeowners to deduct $30\%$ of the gross system cost from their federal income tax liability.

The Recast Amortization Challenge

Because the ITC is claimed when the homeowner files their annual tax return, there is a delay between the loan signing and when the homeowner receives this $30\%$ cash incentive.

To accommodate this delay, standard solar loans are structured with a promotional period (typically $12$ to $18$ months). During this initial period, the lender calculates your monthly payment assuming you will eventually receive the $30\%$ tax credit and pay it directly into the loan.

At the end of this promotional period, a process known as Recasting occurs:

- Scenario A (Credit Applied): If the homeowner pays the full $30\%$ tax credit amount into the principal before the deadline, the loan principal drops to the target level. The monthly payment remains at the low, promotional rate for the rest of the term.

- Scenario B (Credit Retained): If the homeowner keeps the tax credit cash for other personal expenses and fails to pay it into the loan, the lender recasts the loan based on the higher remaining principal. This causes the monthly payment to permanently jump to a higher tier.

Mathematical Formulation of a Loan Recast Jump

To understand this increase, we can calculate the permanent monthly payment increase if the tax credit is not applied.

Let $C$ represent the tax credit that was not applied.

Let $n_{\text{remain}}$ represent the remaining months left on the term after the recast deadline.

Let $r$ represent the monthly periodic interest rate.

Let $K_{\text{recast}}$ represent the adjusted growth factor for the remaining term:$$K_{\text{recast}} = (1 + r)^{n_{\text{remain}}}$$

The increase in the monthly payment ($\Delta M$) is calculated as:$$\Delta M = C \times \left( \frac{r \times K_{\text{recast}}}{K_{\text{recast}} – 1} \right)$$

Where:

- $\rightarrow$ $\Delta M$ represents the monthly payment increase.

- $\rightarrow$ $C$ represents the unpaid Tax Credit amount.

- $\rightarrow$ $r$ represents the Monthly Interest Rate as a decimal.

- $\rightarrow$ $K_{\text{recast}}$ represents the adjusted growth factor for the remaining term.

This highlights why homeowners must plan their cash flow carefully. Failing to apply the tax credit to the loan principal can cause monthly financing payments to increase significantly.

Comparative Evaluation of Solar Financing Methods

Homeowners and businesses can choose from several distinct financing structures to fund their solar installations. Choosing the right method depends on your tax situation, capital availability, and desire for asset ownership.

| Financing Parameter | Cash Purchase | Solar Loan | Solar Lease / PPA |

| Asset Ownership | Property Owner | Property Owner | Third-Party Developer |

| Upfront Capital Required | High ($100\%$ of cost) | Low (Down payment only) | Zero down typical |

| Tax Credit Eligibility | Property Owner | Property Owner | Third-Party Developer |

| System Maintenance | Owner Responsibility | Owner Responsibility | Developer Responsibility |

| Long-Term Savings | Maximized ($100\%$ return) | High (Net of interest) | Moderate (Escalator dependent) |

| Impact on Home Value | Adds equity directly | Adds equity directly | Can complicate home sale |

Real-World Calculation Case Studies

To see how these formulas apply in practice, we can analyze two detailed operational scenarios: a standard residential system with upfront tax credits applied, and a larger premium array with no down payment and an extended loan term.

Case Study A: Standard Residential Solar Array

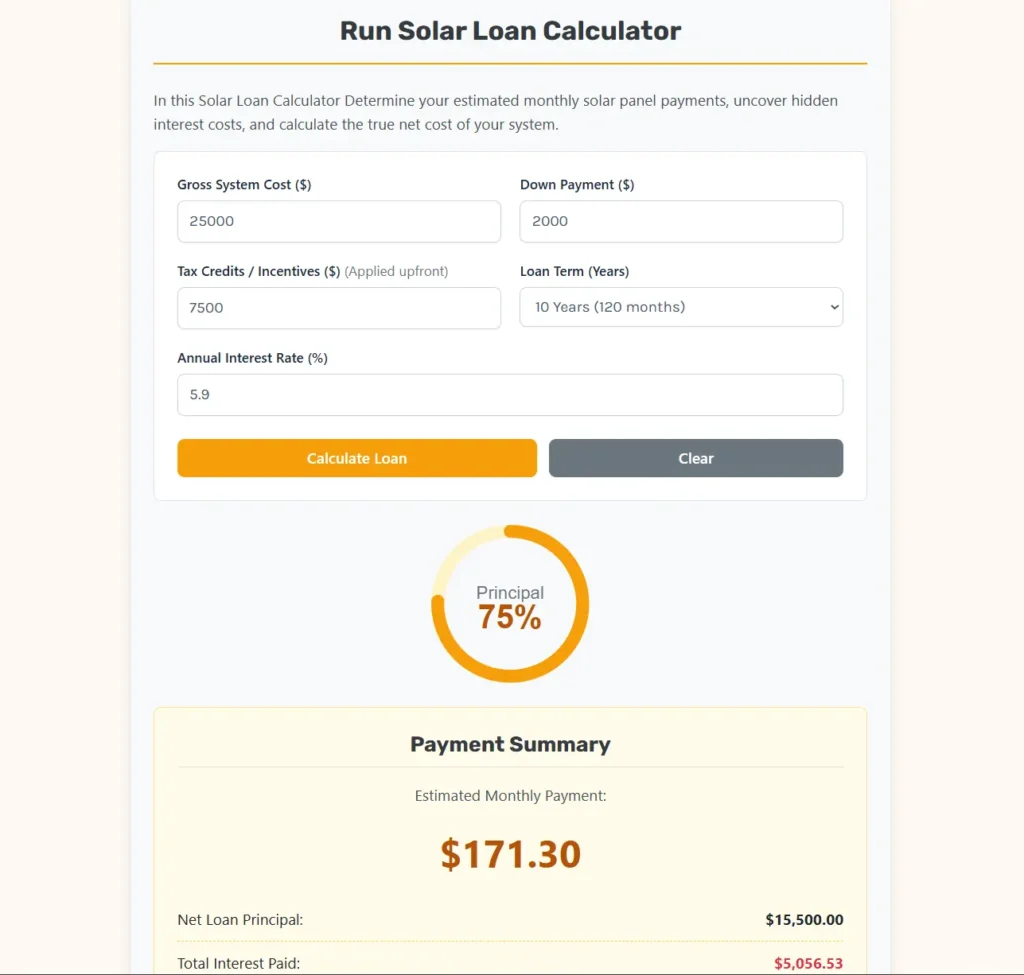

A homeowner purchases a $10\text{ kW}$ solar system for their primary residence.

- $\rightarrow$ Gross System Cost ($G$) = $\$25,000.00$

- $\rightarrow$ Down Payment ($D$) = $\$2,000.00$

- $\rightarrow$ Federal Tax Credit ($C$) = $\$7,500.00$ ($30\%$ of Gross Cost)

- $\rightarrow$ Loan Term ($t$) = $10$ Years

- $\rightarrow$ Annual Interest Rate ($i$) = $5.9\%$

Step 1: Calculate the Net Loan Principal$$P = 25,000.00 – 2,000.00 – 7,500.00$$$$P = 15,500.00$$

Where:

- $\rightarrow$ $P$ represents the Net Loan Principal.

Step 2: Convert Interest and Term into Periodic Monthly Metrics$$r = \frac{5.9}{1200} \approx 0.00491667$$$$n = 10 \times 12 = 120\text{ payments}$$

Step 3: Calculate the Amortization Growth Factor$$K = (1 + 0.00491667)^{120} \approx 1.8021974$$

Where:

- $\rightarrow$ $K$ represents the growth factor of the compound interest.

Step 4: Calculate the Monthly Payment$$M = 15,500.00 \times \left( \frac{0.00491667 \times 1.8021974}{1.8021974 – 1} \right)$$$$M = 15,500.00 \times \left( \frac{0.00886079}{0.8021974} \right)$$$$M = 15,500.00 \times 0.0110456$$$$M \approx 171.21$$

Where:

- $\rightarrow$ $M$ represents the calculated Monthly Payment.

Step 5: Calculate Lifetime Costs and Interest Liabilities$$T_{\text{cost}} = 171.21 \times 120 = 20,545.20$$$$I_{\text{total}} = 20,545.20 – 15,500.00 = 5,045.20$$

The system requires a net loan principal of $\$15,500.00$, resulting in a monthly payment of $\$171.21$ and total lifetime interest costs of $\$5,045.20$.

Case Study B: Large Premium Array with Extended Term

A property owner installs a large-scale solar array with backup battery storage, opting for a zero-down, long-term loan.

- $\rightarrow$ Gross System Cost ($G$) = $\$45,000.00$

- $\rightarrow$ Down Payment ($D$) = $\$0.00$

- $\rightarrow$ Federal Tax Credit ($C$) = $\$13,500.00$ ($30\%$ of Gross Cost)

- $\rightarrow$ Loan Term ($t$) = $20$ Years

- $\rightarrow$ Annual Interest Rate ($i$) = $7.5\%$

Step 1: Calculate the Net Loan Principal$$P = 45,000.00 – 0.00 – 13,500.00$$$$P = 31,500.00$$

Where:

- $\rightarrow$ $P$ represents the Net Loan Principal.

Step 2: Convert Interest and Term into Periodic Monthly Metrics$$r = \frac{7.5}{1200} = 0.00625$$$$n = 20 \times 12 = 240\text{ payments}$$

Step 3: Calculate the Amortization Growth Factor$$K = (1 + 0.00625)^{240} \approx 4.460817$$

Where:

- $\rightarrow$ $K$ represents the growth factor of the compound interest.

Step 4: Calculate the Monthly Payment$$M = 31,500.00 \times \left( \frac{0.00625 \times 4.460817}{4.460817 – 1} \right)$$$$M = 31,500.00 \times \left( \frac{0.0278801}{3.460817} \right)$$$$M = 31,500.00 \times 0.0080559$$$$M \approx 253.76$$

Where:

- $\rightarrow$ $M$ represents the calculated Monthly Payment.

Step 5: Calculate Lifetime Costs and Interest Liabilities$$T_{\text{cost}} = 253.76 \times 240 = 60,902.40$$$$I_{\text{total}} = 60,902.40 – 31,500.00 = 29,402.40$$

Strategic Takeaway: While extending the loan term from $10$ years to $20$ years keeps the monthly payment affordable ($\$253.76$ for a much larger system), it significantly increases the total interest paid. Over the $20$-year term, the interest cost reaches $\$29,402.40$, which is nearly equal to the initial net principal borrowed.

Best Practices for Evaluating Solar Contracts

To avoid hidden costs and maximize your return on investment when signing a solar contract, implement several key practices:

- Identify Hidden Dealer Fees: Many solar lenders buy down the interest rate (for example, offering a promo rate of $2.99\%$) by adding an upfront “dealer fee” directly to the gross cost of the system. Compare cash prices with financed prices to identify these hidden markups.

- Confirm the Recast Rules: Review your loan agreement to find the exact recast deadline (typically month $18$). Ensure you understand when and how to apply your tax credit to prevent your monthly payments from jumping.

- Assess Your Tax Liability: The federal solar tax credit is not a guaranteed cash refund. It is a non-refundable tax credit, meaning you must owe federal income tax during the tax year to claim it. Consult a tax professional to confirm you can fully utilize the credit.

- Match System Lifespan with Loan Term: Solar panels are typically warrantied to perform efficiently for $25$ years. Ensure your loan term does not exceed the warrantied life of your inverters and panels to avoid paying for equipment that needs replacement.

Academic Foundations and Industry References

This guide is built on the core financial theories and solar energy research established by:

- Feldman, D., & Margolis, R. (2018). Solar Photovoltaic Financing: Residential and Commercial Financing Structures. National Renewable Energy Laboratory (NREL).

- For official updates on clean energy tax regulations and federal incentives, consult the US Department of Energy (DOE) solar office database.